Russia and Chelyabinsk See Mortgage Slump in 2025

Mortgage lending in Russia declined in 2025, with fewer than one million housing loans issued, according to the Central Bank of Russia (CBR). This is the lowest level in seven years. A similar situation occurred in the Chelyabinsk region (in the Urals). We examine how mortgage demand changed, the money involved, and discuss with experts how new realities will affect housing prices and sales in 2026.

Average term exceeds 26 years

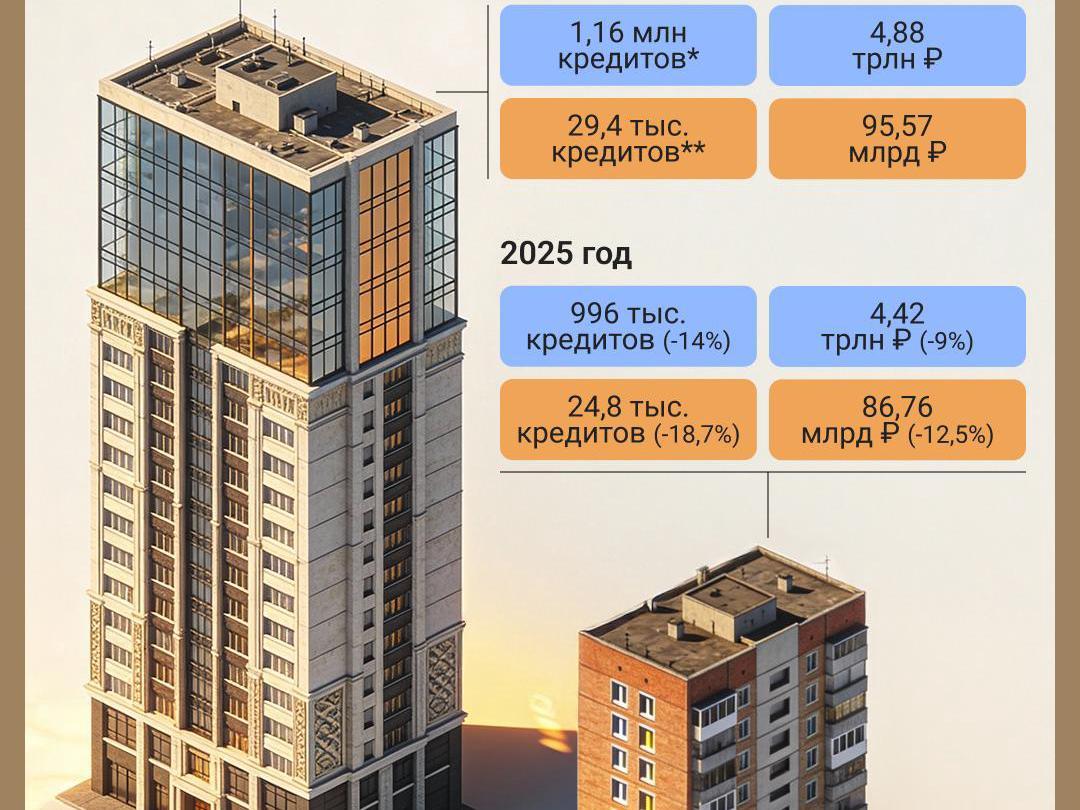

Russian banks issued 996,000 mortgage loans totalling 4.42 trillion rubles (US$49,111,111,100 at current rates) last year, according to the United Credit Bureau (OKB), citing data from the Central Bank. In terms of units, this is the lowest in seven years, and in volume, the lowest in six years. Compared to 2024, the number of mortgages decreased by 14%, while in monetary terms, the decline was slightly smaller — 9% — «thanks» to rising housing prices.

«A surge in mortgage lending was recorded in December, with Russians taking out the maximum number of loans — 162,800. This is 148% more than in December 2024,» the United Credit Bureau noted. «The volume of mortgage loans issued in December was also a record — growing to 776.8 billion rubles (US$8,631,111,100 at current rates).»

At the same time, the average mortgage term in the country exceeded 26 years for the first time in 2025. A year earlier, Russians took out such loans for an average of 25 years and four months.

Residents of the Chelyabinsk region took out 18.7% fewer mortgages last year than the year before. Banks issued 86.76 billion rubles (US$964,000,000 at current rates) to Southern Urals residents for housing purchases, down 12.5% year-on-year. On average, residents took out mortgages of 3.3 million rubles (US$36,700 at current rates), with the average loan term reaching 249 months (about 21 years).

Deposits went toward housing purchases

The past year showed a consistent recovery in mortgage lending, experts noted.

«After the January low, virtually every month the market grew at least a little, ending the year with a 50% increase in December. The main driver was the easing of monetary policy. Lower market mortgage rates enabled those borrowers for whom buying a home was a critical issue and who had sufficient income to afford high mortgage payments to approach property purchases,» explained Mikhail Aleksin, CEO of the United Credit Bureau. «Also, the demand from borrowers who in 2024–2025 preferred a savings strategy and placed savings in deposits until better times began to materialize. As annual deposits matured toward the end of 2025, people chose to buy housing without waiting for another round of price increases.»

The peak in mortgage lending in December is, of course, linked to record disbursements of loans for housing purchases under preferential programs, the head of the United Credit Bureau added.

By the way, the traditional scenario of «December frenzy — January lull» did not work this year.

«Clients who did not manage to close a deal at the end of the year completed it in January. Others, who had been deliberating, made a final decision. As a result, a unique January peak formed, covering Russia no less than the anomalous snowfalls,» noted Alexey Okhorzin, Senior Vice President and Head of Retail Business Products at VTB. «This shift will certainly affect February statistics, but after a short pause, we expect the market to return to sustainable growth.»

«Maternity capital served as a down payment»

The situation in the Chelyabinsk region matches the nationwide trend, agreed mortgage broker Kirill Pavlov. According to him, the main common problem is that market mortgage rates were and remain high.

«Transactions on the secondary market were mostly by people with a large down payment. They covered only the remainder with a mortgage loan,» explained Kirill Pavlov.

The most popular were, of course, preferential programs, primarily family mortgage.

«A rate of 6% with a maximum loan amount of 6 million rubles for a 30-year term and a monthly payment of 36,000 rubles is quite comfortable for purchasing a two-room apartment. There is demand for two-room apartments. For that money, you could buy housing with a minimal down payment, which often came from maternity capital,» stated Kirill Pavlov.

From 1 February 2026, the conditions changed of the «family» mortgage. Now both spouses must be co-borrowers; children must be registered at the same address as the borrower; and it is prohibited to attract families with children as co-borrowers if they are not themselves buying housing.

Market participants still expect a systematic reduction of the key rate, after which rates on all loans, including mortgages, will be revised.

«The market rate for a standard mortgage is typically 3–3.5% higher than the key rate. Accordingly, if the key rate is 13%, mortgage rates will drop to 16–16.5% per annum,» the mortgage broker suggested. «That is already more or less comfortable conditions for buying housing on the secondary market without preferential programs. As for family mortgages, due to the tightening, a decline in lending volume is possible.»

At the same time, in the second half of the year or closer to the end of 2026, the expert hopes for an increase in mortgage transactions on the secondary market.

«The same effect as with cars»

Prices in statistics from aggregators, which seem to rise constantly, are not entirely accurate, the expert noted.

«In the past couple of years, a large number of new buildings in the economy and comfort segments were handed over, and they were 40–50% more expensive than secondary housing. After occupancy, the same effect occurs as with cars: as soon as a car leaves the dealership, it loses 30% of its value. But they try not to take this effect into account in average figures. And these inflations prevent adequate work with mortgages — no one will buy an apartment worth 10 million for 12–13 million,» gave an example Alexey Krichevsky, financial expert and author of the Telegram channel «Economism».

«The curtailed family mortgage no longer holds the same interest as, for example, three months ago, when developer offices suddenly filled with buyers. Consequently, a greater number of loans can only be achieved through lower rates and dumping, which is simply impossible in current realities,» added Alexey Krichevsky.

In addition, with the increase in the number of «bad» debts, scoring (a borrower assessment system used by banks and microfinance organizations to evaluate risks when issuing loans — Ed.) will tighten. This means that the number of approved applications, which already falls to 20% in some places, could decline even further, or banks will offer deliberately unrealistic conditions.

Now, according to the expert, everything depends on how the CBR rate moves further.

«If we see 12% or lower by the end of the year, then in the fourth quarter there could be a surge in activity from borrowers who remain sufficiently solvent for a loan at 15+% per annum. But there are fewer and fewer borrowers with such a «liquidity» cushion every day due to soaring inflation and closing companies,» emphasized Alexey Krichevsky. «Therefore, a good result for banks, as it seems now, would be to repeat last year«s results. A decent result would be a slight decline to around 900,000 loans issued.»

«Prices will show moderate growth»

Record-low mortgage lending volumes in 2025 marked the transition of the housing market to a new, tighter phase, experts emphasized.

«The reduced availability of family mortgages, the high cost of market loans, and the general cooling of demand already hit the number of transactions in 2025. In 2026, these factors will continue to shape market dynamics. Housing sales will most likely remain below the levels of 2023–2024, while the structure of demand will shift towards wealthier buyers and transactions without mortgages,» stated Yaroslav Kabakov, Director of Strategy at IC Finam.

The primary market will maintain relative stability, but even there, according to the expert, sales rates will slow.

«The tightening of family mortgage conditions will cut off part of mass demand, and developers will increasingly compensate for the decline in credit availability through installment plans and their own subsidies. This will avoid a sharp collapse but will not return the market to previous volumes,» noted Yaroslav Kabakov. «The secondary market and suburban real estate look more vulnerable: here demand directly depends on market mortgages, and with high rates, buyers prefer to postpone transactions or switch to renting.»

We asked experts how the new realities — reduced availability of family mortgages, overall price increases, stagnation of the secondary and suburban real estate market — will affect prices and demand for apartments in 2026.

«In new buildings, prices will most likely remain stable or show moderate growth due to high construction costs and developers« reluctance to directly cut prices,» Yaroslav Kabakov is confident. «On the secondary market, stagnation is likely, and in some regions, a careful downward correction, especially with excess supply and weak demand. In the largest agglomerations, prices will hold up better due to solvent demand and limited quality supply.»

According to the expert, mortgages will remain a key constraint on demand, and without a significant reduction in rates or an expansion of state support programs, a rapid increase in sales cannot be expected. The market will operate in a mode of low turnover, moderate price fluctuations, and increasingly noticeable stratification between segments and regions.