Mortgage programs drive five waves of demand in St. Petersburg new-build market

Specialists from GC PSC, having studied open Dataflat data for 2023-2025, concluded that the primary real estate market in St. Petersburg experienced five waves of demand over three years. Its dependence on mortgage lending significantly intensified during this period.

Throughout this period, mortgage conditions were progressively tightened. A mass preferential program was first restricted and then canceled, the IT mortgage program in St. Petersburg was discontinued, and conditions for the family mortgage were adjusted. All this occurred against a backdrop of sharp fluctuations in the Central Bank«s key rate — from 7.5% to 21%, followed by a reduction to 16% per annum.

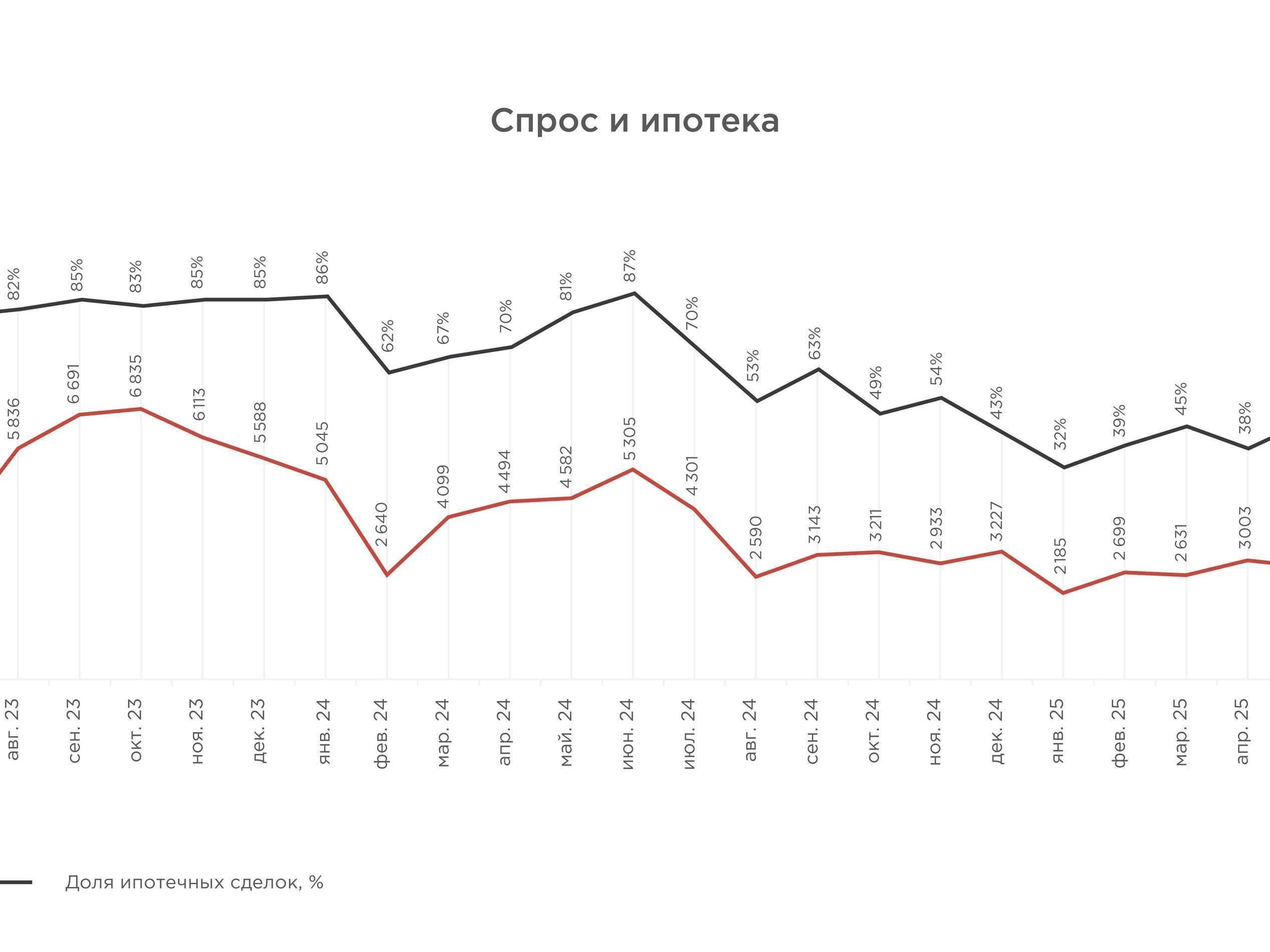

The average share of mortgage-backed transactions decreased from 85% in 2023 to 65% in 2024 and 46% in 2025. Sales volumes in monetary terms also declined simultaneously:

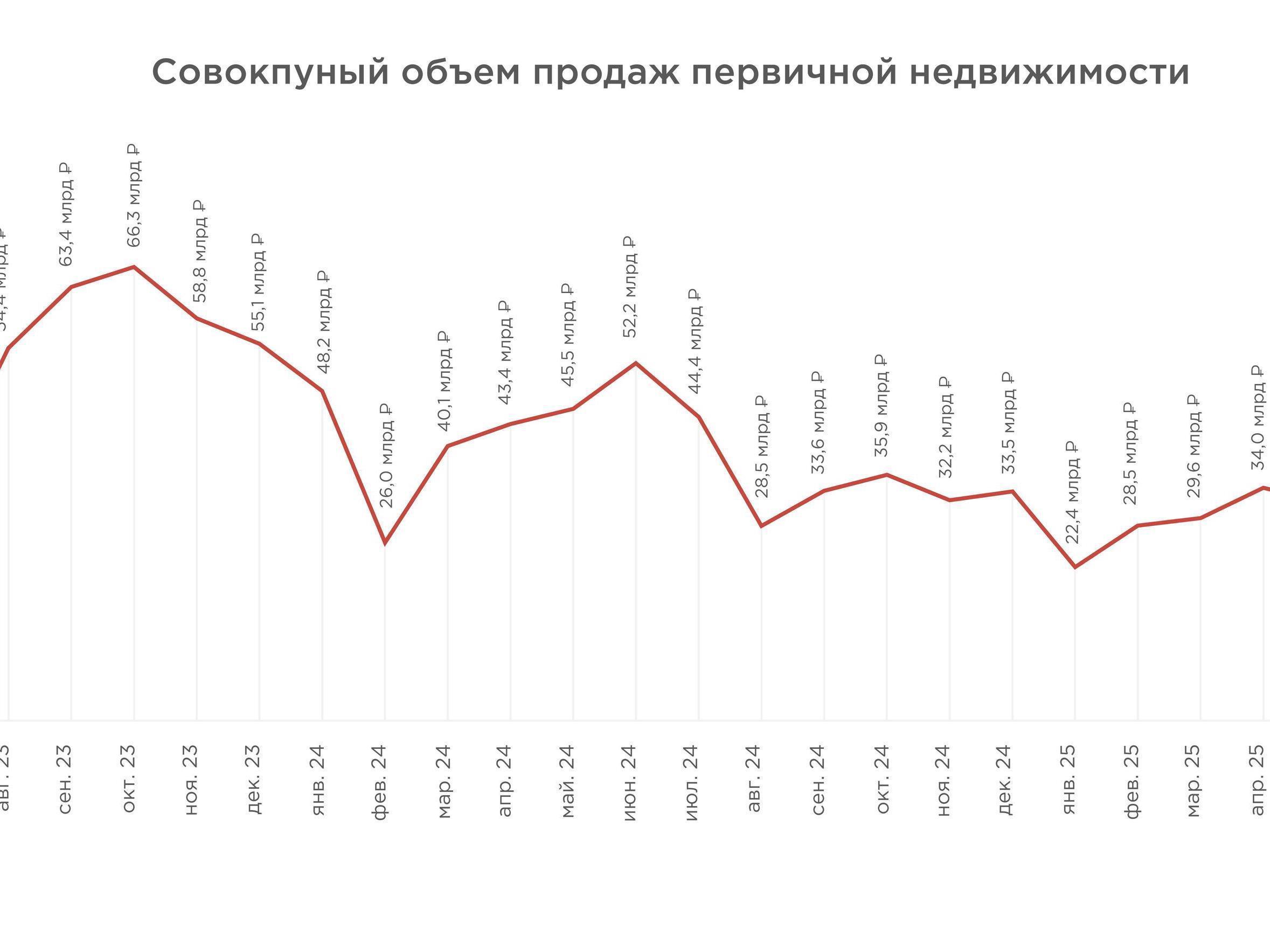

- 2023: 525 billion rubles (approx. $5.8 billion at current rates)

- 2024: 463 billion rubles (approx. $5.1 billion at current rates)

- 2025: 441 billion rubles (approx. $4.9 billion at current rates)

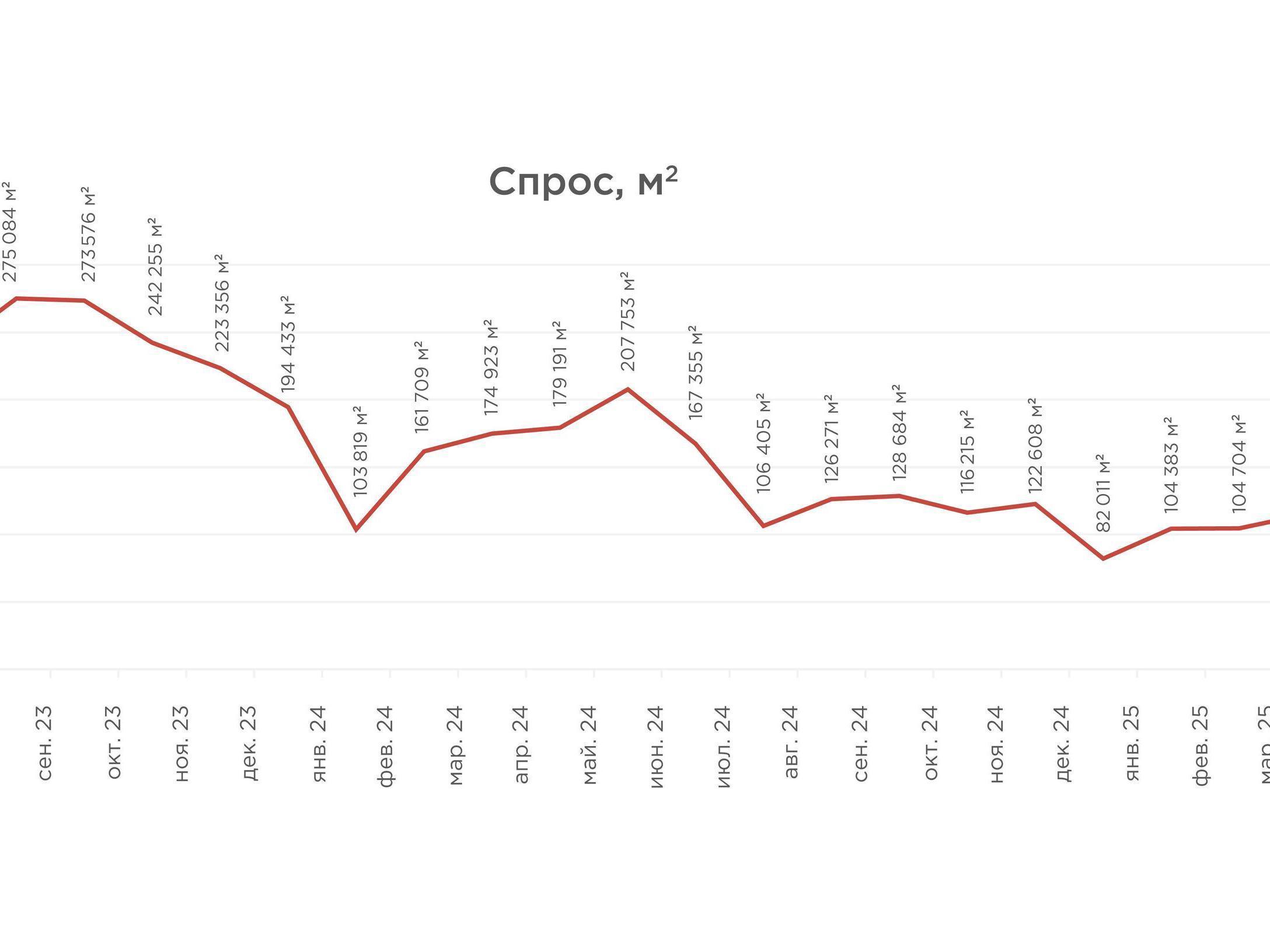

In terms of area, sales dropped from 2.27 million sq. m to 1.8 million sq. m and 1.5 million sq. m respectively.

The average area of purchased apartments decreased from 41.2 sq. m (approx. 443 sq. ft) in 2023 to 39.4 sq. m (approx. 424 sq. ft) in 2024 and 38.6 sq. m (approx. 415 sq. ft) in 2025. At the same time, the price per square meter increased by 41% over three years — from 224 thousand rubles to 316 thousand rubles.

Commercial Director of GC PSC Sergey Sofronov cited the main reasons for the price increase: rising costs of construction and installation work, increased costs of project financing due to higher interest rates, and growing social obligations within project costs.

The peak month during the analyzed period was October 2023 with sales of 66.3 billion rubles (approx. $732 million at current rates). December 2025 nearly reached this level at 63.6 billion rubles (approx. $703 million at current rates). Such a surge at the end of 2025 is explained by the rising average price per square meter, high demand for family mortgages (its terms are set to change from 1 February 2026), and the traditional seasonal uptick. Compared to December 2024, sales in December 2025 grew by 60% in area and 81% in monetary terms, indicating frenzied demand.

Monthly analysis revealed four completed demand waves, each weaker than the previous in terms of peak values and duration. The fifth wave, which began in the second half of 2025, proved atypical: its peaks sit between the previous ones, and the November decline was followed by a sharp December spike thanks to the family mortgage and seasonal factors.

The correlation between demand and mortgages has significantly strengthened. In 2023, the share of mortgage deals stayed at 80-86%, while the number of deals fluctuated from 2.6 to 6.8 thousand per month; the correlation coefficient was 0.47, indicating a moderately weak link. From February 2024 through the end of 2025, the curves for demand and mortgage issuances nearly coincided, and the correlation coefficient rose to 0.83, signaling a very strong dependency. According to GC PSC, the family mortgage accounted for 85-90% of all mortgage deals during this period.

The company notes that key market trends are now determined by mortgage program conditions, while rising construction costs remain the primary factor for price increases. The market is currently entering a downward phase of the latest wave, which will become more noticeable from February. Analysts expect renewed activity in spring due to pent-up demand.

The forecast for 2026 is assessed as cautiously positive. «Further sales dynamics have a chance to remain moderately positive after a dip in the first quarter — thanks to a decrease in the Central Bank»s key rate and lower market mortgage rates,« noted Sergey Sofronov. »At the same time, there are no visible prerequisites for a reduction in the cost per square meter.«

Sofronov also highlighted two opposing buyer approaches: some are adopting a wait-and-see position, hoping for better mortgage terms while ignoring the prospect of price increases. Others prefer not to postpone their purchase to avoid further price hikes, planning to refinance later.